Excitement around the private equity asset class seems to be at a fever pitch. As of the start of 2019, there were roughly 3,800 active private equity and private capital funds targeting nearly $1 trillion in capital. If you look at “dry powder” — funds that have been raised but have not yet found a home — that number ticks up to more than $2 trillion. Tax-exempt organizations are contributing a significant portion of those private capital investments.

This level of activity has a dark side, however. When people hear about outsized outcomes, such as the windfall returns reaped by a Bay Area private school on its early-round investment in Snapchat, they tend to flood the asset class. And too many dollars chasing too few deals end up driving down investment returns.

So, should your nonprofit invest in private capital? And if so, what is the best approach to manage the opportunities, challenges and risks inherent in the asset class?

Why Allocate Funds to Private Capital?

A balanced portfolio includes allocation to a variety of asset classes — from fixed income to public and private equity — that entail a range of risks and expected returns. The right balance for any organization depends on its objectives (such as portfolio growth, capital preservation or protection against inflationary periods) as well as its particular constraints (such as time horizon, risk objectives, spending needs and available liquidity).

For organizations seeking long-term portfolio growth, private equity is an attractive option. Some merits of private capital include:

Long-term outperformance against public markets. Private equity has consistently outperformed the S&P 500 over the long-term (10 years or more). Over the past 15 years, private capital has earned roughly 4 percent more than the S&P 500, according to Q1 2018 data from the Cambridge Associates LLC US Private Equity Index. Going back 20 years, that premium grows to roughly 5.5 percent.

Access to high-growth companies. The asset class includes a large proportion of high-growth companies, such as those in developing industries and technologies.

Greater control over returns. Compared with investors in public equity and many other asset classes, private capital investors are less dependent on factors they can’t control — such as market fluctuations. By strategically investing with certain types of managers and funds focusing on operational value-adds, private capital investors can maintain greater control over the funds’ returns.

Managing Private Capital Investment

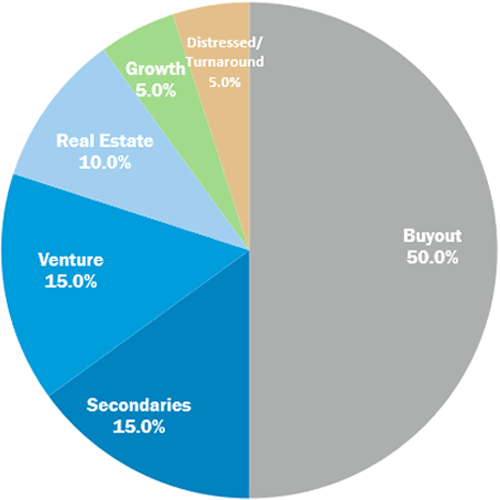

Nonprofits allocating part of their portfolio to private capital should aim for diversification within the asset class among the key subsets of the market. These subsets include:

Construction - Allocation

Source: Canterbury Consulting

Buyout. Acquisition of a controlling interest in companies.

Secondaries. Primarily purchasing existing investor commitments to private equity funds, generally at a discount.

Venture capital. Focus on startups and early-stage companies with long-term, high-growth potential.

Real estate. Includes the development, acquisition, financing and ownership of real estate properties.

Growth. Usually a minority investment in relatively mature companies seeking capital to expand or restructure operations.

Distressed/turnaround. Targeting companies experiencing distress such as liquidity, capitalization or underperformance issues.

The actual returns realized within each asset subclass can vary dramatically from year to year, making diversification important to managing the growth of the portfolio. Returns in the buyout subclass are generally the most stable (i.e., predictable), which is why investment managers tend to recommend allocating the greatest share of private capital investment to that subsector. More volatile subclasses, such as venture capital, typically receive smaller portions.

Just as important is the pace at which investments are made. Ideally, private capital investment strategies are multiyear plans. Investors make commitments, and those investments are “called down” over time as opportunities become available. This methodical pace lets investors use the market’s volatility to their advantage — reaping the returns of the highest-performing subclass in each year while insulating the portfolio somewhat from potentially subpar returns in other subclasses. Over several years, the portfolio achieves the target diversification while returns from prior years fund new commitments rather than requiring capital calls.

Use Caution: Challenges and Risks of Private Capital

It’s important to enter any investment with eyes wide open regarding the challenges and risks. With private capital, those risks include:

Illiquidity. Make sure your intended investments match your organization’s investment philosophy. Private capital investments lock up assets for long periods — often 10 years or more. Can your investment portfolio withstand this period of illiquidity? If your investment committee has a high rate of turnover — a common situation with private schools and other nonprofits — will the next group of committee members feel comfortable with the investment allocation?

Ongoing management of capital calls and distributions. This isn’t your traditional investment, where you set it and forget it. Ongoing management is required to track the capital calls, distributions and unfunded commitments.

Manager selection. These are more expensive investments, which entail higher fees and have a wide dispersion of returns between top- and bottom-quartile funds. Manager selection is essential to performance in a private capital portfolio. Look for a manager with a strong track record. Although past performance does not guarantee future returns, the manager should have a clear, repeatable investment strategy. You also want a manager with relationships and access to the right funds. With so many dollars chasing this asset class, access to the right funds is critical.

Accounting and Financial Reporting Implications

In addition to the risks covered above, private capital investments require some specific accounting and reporting considerations:

Additional accounting processes. Private capital investments result in specific fund statements, year-end valuations and off-year reporting requirements. Make sure you have the repeatable processes in place to recognize the activity appropriately on your financial statements.

Unrelated business income tax. Don’t get caught flat-footed — some of these private capital investments are structured in a way that may trigger UBIT to tax-exempt investors. To the extent those investors have net income from the activities, they may owe tax.

New liquidity reporting requirements. Given the illiquid nature of private capital investments, nonprofits considering entering the asset class (or expanding their presence) should be mindful of the new FASB nonprofit reporting standard (FASB ASU 2016-14) and its liquidity disclosure requirements. Make sure you’re telling the right story in your financial statements, with proper quantitative and qualitative information about how your nonprofit is managing its liquid available assets and its liquidity risk.

Many foundations, private educational institutions and public charities are reaping the benefits of private capital investments — which can include operating income flexibility, expanded geographical presence, endowment growth and improved mission impact. However, investments should only be made with a clear understanding of the risks and complexities involved. Consult with your investment and accounting advisors to help you make decisions that will achieve your nonprofit’s objectives.