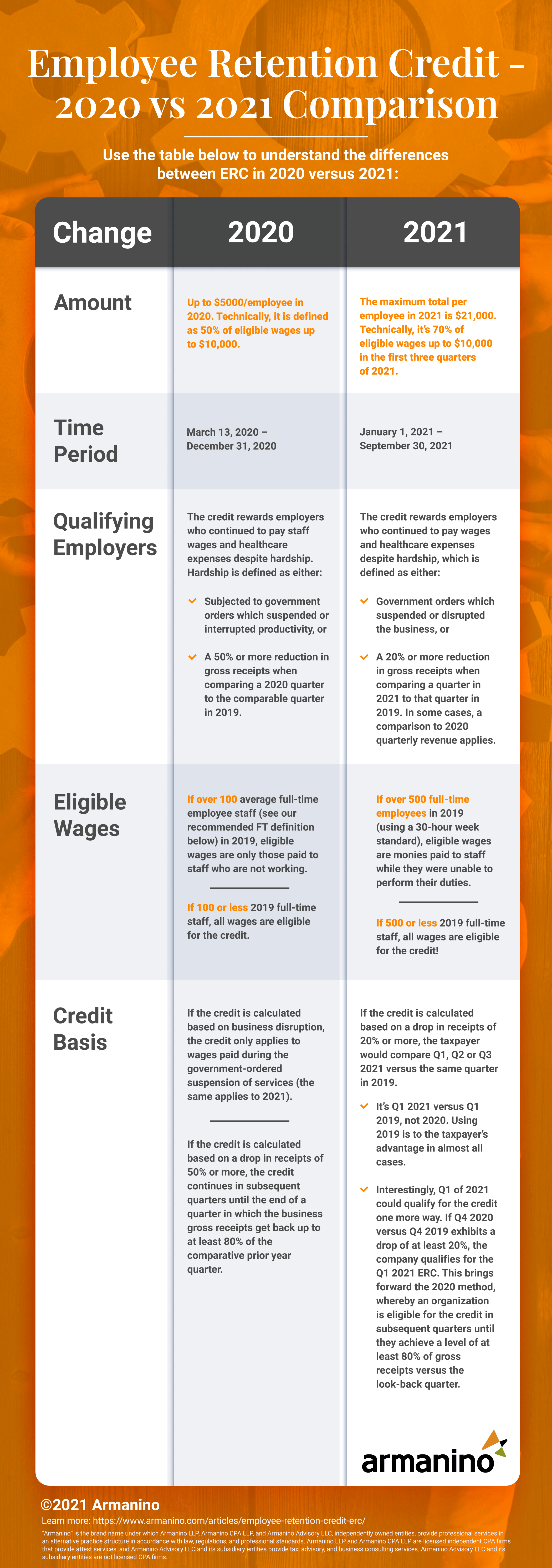

This ERC is explicitly meant to help employers that suffer financial losses, but still continue to pay workers who are unable to perform their duties. It, like other CARES Act measures, rewards employers that keep employees on the payroll, making it an important consideration from both a Business Tax and Employment Law perspective.. This credit is available for payroll from March 12 to December 31, 2020.

The retention credit is a tax credit — not a deferral — against federal employer taxes. This credit is measured quarterly. If the credit applies, taxes are completely waived.

The Infrastructure Investment and Jobs Act, enacted on November 15, 2021, amended section 3134 of the Internal Revenue Code to limit the Employee Retention Credit only to wages paid before October 1, 2021, unless the employer is a recovery startup business. This regulatory update was crucial in redefining the scope of the credit and ensuring compliance with the new legislative framework.

IRS issued guidance regarding the retroactive termination of the Employee Retention Credit.

There are certain stipulations that can impact qualification such as a complete business shutdown, a decline in quarterly gross receipts meeting defined thresholds, or a partial suspension of operations due to a government order. Refer to the specific sections for more information.

When the CARES Act was passed, it created both the SBA Employee Retention Credit (ERC) program and Paycheck Protection Program (PPP). They were mutually exclusive, but the Consolidated Appropriations Act (CAA), which was signed into law on December 27, 2020, significantly expanded the ERC and allows employers who borrowed PPP loan funds to take advantage of both programs. This change represents a major Tax Update for eligible businesses.

There are several exciting developments regarding ERC which include, it’s refundable. That means you get a refund if the credit exceeds the amount of Social Security taxes withheld. It’s a dollar-for-dollar credit against employment tax. Businesses losing money may not owe much income tax, but they often employ people and incur payroll taxes. It’s instant cash relief. You can get the credit in advance of filing your quarterly payroll returns if you’re certain that you’ll qualify and the credits are big.

A close reading of these new provisions also reveals wages used for the ERC calculations take precedent over wages used in PPP math. That raises questions for taxpayers who have already filed for PPP forgiveness.

Want to display this infographic on your site? Copy and paste the following code. Be sure to include attribution to armanino.com with this graphic.

There are three ways to qualify for the Employee Retention Credit (ERC). Two are relatively straightforward, and one is complex and subject to interpretation. An organization may qualify if there is

It's the third qualifier we are concerned with: If you recently received a call or email informing you that you could get $26,000 per employee in COVID Aid, you should be wary. Each entity should have eligibility evaluated on its own merits. The process is complex, and documentation is more rigorous. Sweeping generalizations about eligibility are aggressive and unwise.

To qualify using the argument an organization was partially suspended, at some time between March 13th 2020 and September 30, 2021, the following is required:

Interestingly, the IRS has not yet indicated what they’ll do when reviewing an ERC for an organization that does not meet the 10% safe harbor. It’s logical to assume the writers of this legislation and subsequent guidance will expect to see proof of more than nominal negative impact. Therefore, showing shut-down orders alone, unaccompanied by proof of adverse financial impacts, could be problematic in an audit where material amounts of a credit have been claimed. Organizations that did not suffer a revenue or profit decline are strongly advised to prepare evidence of the adversity experienced via an analysis of hours worked in segments of the business in 2019 that were clearly not operable during pandemic periods.

We all know that legislators and the IRS are aware of abused COVID Relief programs. The government has indicated recently that enforcement activity will commence, and it will be aggressive. As audits begin, we can expect further clarity on what is considered acceptable documentation when claiming the ERC due to a partial shut-down of operations.

For anyone excited about reading it, the IRS provides hundreds of pages of examples in Notices 2021-20, 2021-23, 2021-33, and 2021-49.

In order to claim the new Employee Retention Credit, eligible employers will report their total qualified wages and the related health insurance costs for each quarter on their quarterly employment tax returns, which will be Form 941 for most employers, beginning with the second quarter. The credit is taken against the employer's share of Social Security tax but the excess is refundable under normal procedures.

Eligible employers can also request an advance of the Employee Retention Credit by submitting Form 7200. Taxpayers can file it more than once a quarter. However, the IRS has rejected many 7200s, and we do not always recommend an advance credit filing. Claim the credit on a Form 941, which is the federal quarterly payroll tax return. If filing after the due date, a 941-X can be filed to amend the return.

The following examples might help clarify (assuming either there is a government order or a drop in receipts to qualify):

The following will help clarify or avoid pitfalls within the ERC regulations.

On September 14, 2023, the IRS announced a moratorium on processing new ERC claims through at least the end of 2023 (the IRS has not set a definitive end date). The moratorium was in response to aggressive marketing scams that have arisen through TV, radio, texts, mail (ads that look like official government letters), phone calls, and social media.

The IRS is also collaborating with the Justice Department to combat fraud, safeguard against abuse and protect businesses from predatory marketing tactics.

While the IRS continues to process claims from organizations that have already filed for the ERC, the processing timeline has slowed drastically due to the complex nature of these filings and the need to prevent improper payments.

If you think you were affected by the ERC scams or need a hand reviewing your ERC filing, we are here to help. Reach out to our Employee Retention Credit experts about what to do next.

In December 2023, the IRS launched the ERC Voluntary Disclosure Program. This innovative solution allows employers who have received ERC refunds to return a portion of them and avoid penalty.

Update August 20, 2024: The IRS has opened a second Employee Retention Credit (ERC) Voluntary Disclosure Program for a limited time. If you still need to correct a previous ERC claim, you have a window of opportunity to avoid penalties and interest.

Through the second ERC Voluntary Disclosure Program (ERC-VDP), the IRS is allowing businesses that received ERC refunds for 2021 tax periods and are not currently under investigation to return a portion of the refunds and avoid penalties.

Note: If you received an ERC refund for 2020 tax periods, you can no longer apply for the ERC Voluntary Disclosure Program.

If you believe you may qualify for the second phase of the ERC-VDP, our team of ERC experts is here to help you review your ERC claims.

The proposed Tax Relief for American Families and Workers Act of 2024 would end the ERC program effective January 31, 2024, to clamp down on fraudulent payments of the COVID-era tax credit. If this tax package passes, businesses would not be able to submit ERC claims after January 31, 2024.

The bipartisan legislation was passed by the House on January 31 and next moves to the Senate for consideration.

Approach the ERC process methodically, using a well-coordinated team comprised of HR, payroll and tax professionals.

Navigating the ERC application process can be daunting, and you may be wondering if your business still qualifies — or if recouping funds is still even possible. But if you’re a small business owner that is ERC-eligible, you can still claim credit for revenue lost in 2021.

This ERC checklist outlines some key considerations as you determine your eligibility and apply for the credit.

If your ERC refund has not yet been received, the IRS recommends the payroll tax return amendment, Form 941X, should be amended or rescinded. There is a specific process for entirely reversing the 941X. If the refund amount was miscalculated, a new amended Form 941X must be filed.

We’re here to help! For questions or assistance with ERC, contact our tax credit experts.

Armanino has the industry expertise, tax credit experience and track record of customer satisfaction to best advise your tax credit incentive strategy and compliance needs.

Contact us today for a free assessment.