What you need to know about OZ tax benefits.

Opportunity zones (OZ) reward long-term capital commitments in distressed communities with significant tax advantages — but the One Big Beautiful Bill Act (OBBBA) legislation is reshaping the rules:

Opportunity zones (OZ) are federally designated low-income areas that offer special tax incentives for investment in qualified local businesses and property.

Also known as a “Qualified Opportunity Zone” or QOZ, the designation was created by the 2017 Tax Cuts and Jobs Act to encourage long-term, private investment in economically distressed communities. While the program was originally set to expire in 2028, it was made permanent by “The One Big Beautiful Bill Act” (OBBBA) which was signed into law in July 2025. This retains many of the tax advantages but also has new requirements and considerations starting in 2026.

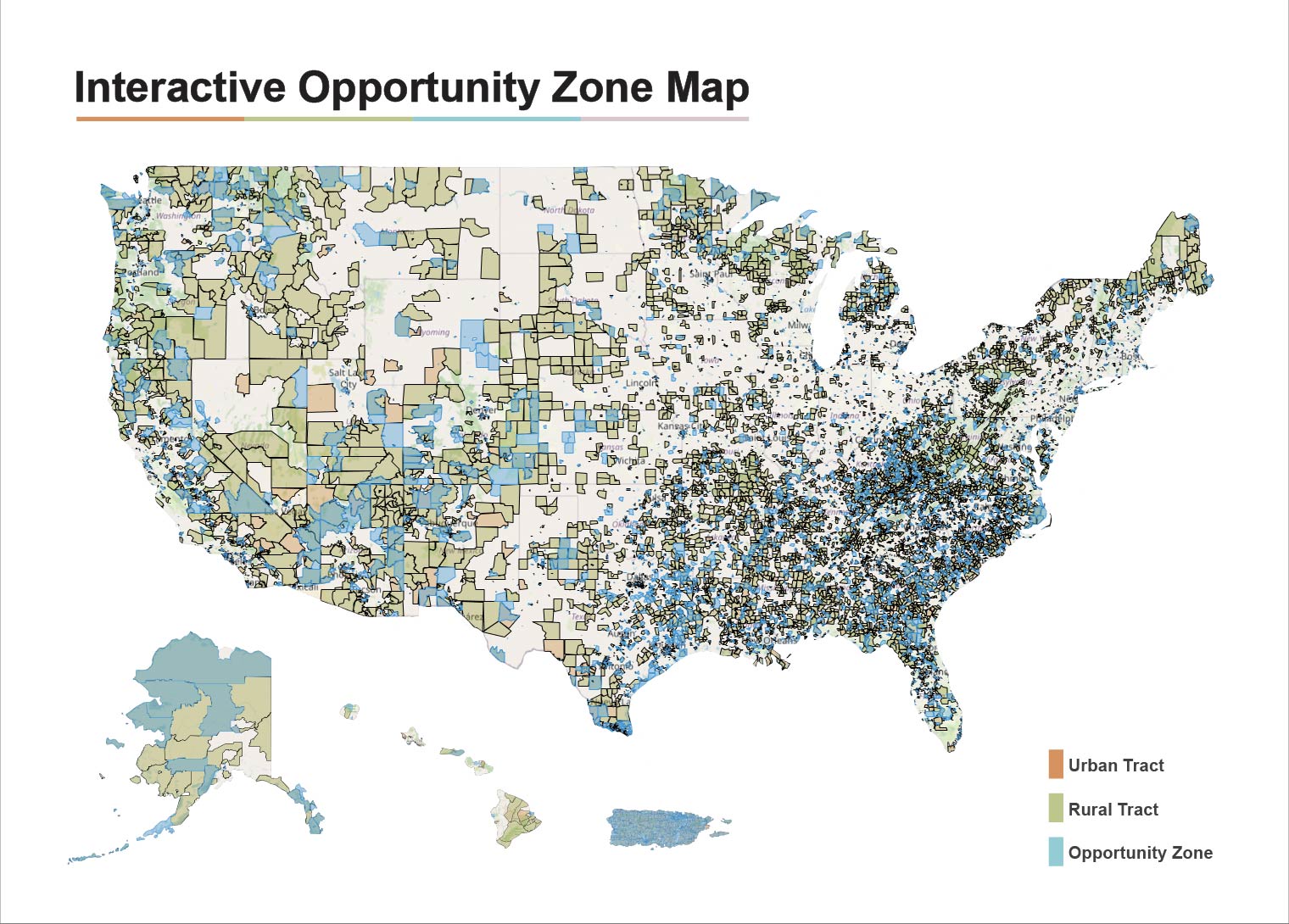

As of the original 2017 designation, there were 8,746 opportunity zones in the United States and U.S. Territories. There are about 7,000 under the changes enacted by the OBBBA that affect zone eligibility and designation. For a closer look, explore the interactive Opportunity Zone Map1 and stay informed by subscribing to map updates.

At the end of 2026, the OBBBA will sunset the current set of OZs and create a new set of zones starting in Jan. 2027. The newly revised tax benefits, including the capital gains deferral, will only be available after Jan. 1, 2027, for investments made in the newly designated zones.

The OBBBA also has stricter eligibility criteria and narrows the set of census tracts eligible for designation as OZs. There are several notable changes:

See the official HUD Opportunity Zone website for additional detailed resources.

Several states, including California, Massachusetts, Mississippi, North Carolina and Washington state, do not conform to the federal opportunity zone tax rules and offer their own state-level tax breaks. So, investors from these states only benefit from the federal program. In those states that conform to the federal opportunity zone tax rules, the applicable capital gains tax for both federal and state is deferred and avoided.

Opportunity zones offer tax benefits to individuals or corporations who reinvest short-term or long-term capital gains in a Qualified Opportunity Fund (QOF). To receive the maximum tax benefit, the gains must remain invested in the QOF for at least 10 years.

Opportunity zone designations were originally set to expire at the end of 2028, with investors having until 2047 to dispose of their QOF investment. However, the OBBBA made the opportunity zone program permanent.

Claiming OZ benefits requires two IRS forms. Form 8997 must be attached to the investor's tax return each year the investment remains in a QOF. IRS Form 8949 is required in the first year to report the capital gain and flag the deferral election. Beneficiaries of trusts or estates also file Schedule K-1 (Form 1041).

The OZ program delivers three distinct tax advantages — each more powerful the longer capital stays invested.

Investors don’t pay tax on deferred gains until Dec. 31, 2026, or when they dispose of the asset, whichever is earlier. For investments made after Jan. 1, 2027, in the newly designated zones, investors defer the original gain until the Qualified Opportunity Fund (QOF) is disposed of or the inclusion event occurs.

When an investment is kept in a QOF for at least 10 years, there is no tax on capital gains that accrued after the investment.

There is now a new tiered structure for investments in rural areas and non-rural areas.

“Rural areas” are defined in Notice 2025-50 as any area other than a city or town with a population greater than 50,000 and excluding urbanized areas contiguous to such cities. Those who invest in rural OZs and hold them for five years receive up to a 30% reduction in the capital gains tax owed on the deferred gains. As of IRS Notice 2025-50, 3,309 OZs were located entirely in a rural area.

Those who invest in non-rural OZs and hold them for five years receive up to a 10% reduction in the capital gains tax owed on the deferred gains.

The OBBBA also offers additional benefits for property improvements in qualified, entirely rural OZs. As of July 4, 2025, the improvement threshold was reduced from 100% to 50%. Under the new threshold, investors must invest an amount equal to 50% of the building's cost basis — excluding land — rather than the previous 100% requirement. That lower bar makes it significantly easier to qualify existing rural buildings as opportunity zone property.

A QOF is a corporation or partnership structured specifically to deploy capital into opportunity zones. That 90% threshold is calculated by averaging asset percentages at the midpoint and final day of the QOF's tax year.

A QOF must file IRS Form 8996 with its annual federal income tax return. While QOFs can directly own a Qualified Opportunity Zone (QOZ) business property or invest in qualified opportunity zone businesses, they cannot invest in another QOF.

Tangible property owned by a QOF must meet these requirements to qualify:

Leased property used by a QOF must also be considered in its 90% test, even though leases and leased property are generally not valued or reported as assets for tax purposes.

The value is determined by discounting the present value of future lease payments using the IRS Applicable Federal Rate (AFR). Once the lease is initially valued (when it is entered into), its value remains unchanged for all subsequent testing dates. If a QOF has an Applicable Financial Statement that reports leased property as assets, the value can be used if it is also used in calculating the value of tangible property owned.

An investment in a QOF must be an equity interest, including preferred stock or a partnership interest with special allocations and debt instruments do not qualify. However, investors can use a QOF investment as collateral for a loan.

Investors have 180 days from the triggering gain event to roll proceeds into a QOF — missing that window forfeits the deferral benefit.

To qualify for deferral, investors must invest in a QOF within 180 days of the sale or exchange that generates the gain or the date that the gain would otherwise be recognized for federal income tax purposes.

For gains from pass-through entities (a partnership, trust/estate or S corporation), the rules generally allow either the entity or the partners, shareholders or beneficiaries to elect deferral.

A QOF has 12 months to reinvest its proceeds from the return of capital or the sale/disposition of property in a qualified opportunity zone property. If the QOF’s reinvestment plans are delayed due to a federally declared disaster, it has an additional 12 months to reinvest.

Qualified Opportunity Funds are tested by the IRS semiannually for rule compliance. The initial testing date is on the last day of the sixth month after the fund’s taxable year begins and the second testing date is on the last day of the fund’s taxable year.

For a trade or business to be a qualified opportunity zone business, at least 70% of its owned or leased tangible property must be qualified opportunity zone business property, and it must comply with specific business tax rules.

A qualified opportunity zone business property is a tangible property acquired by a QOF after 2017 and used in a trade or business.

To be designated as a qualified opportunity zone business, it must meet all of the following tests:

The business is not a private or commercial golf course, country club, massage parlor, hot tub facility, suntan facility, racetrack, gambling facility or any store whose principal business is the sale of alcoholic beverages for consumption off premises.

Armanino has the industry expertise, tax credit experience and track record of customer satisfaction to best advise your tax credit incentive strategy and compliance needs.

Contact us today for a free assessment.