The Tax Cuts and Jobs Act (TCJA) expanded the use of the cash method of accounting to business entities including those with inventories if their average gross receipts are $25 million or less starting with years beginning after January 1, 2018, incorporating recent regulatory updates impacting business tax compliance. The change is adopted by filing Form 3115 with the tax return for the year the change is to apply and may result in a substantial negative amount for the change from accrual to cash that occurs at the beginning of the year of conversion.

If a negative change arises in the conversion from accrual to cash, the loss is subject to two limitations of the TCJA. First, the loss allowed in the current year cannot exceed an excess business loss limitation of $250,000 for single and $500,000 for married taxpayers. Second, any losses in excess of current year income can only be carried forward and are further limited to offsetting only 80% of the future year’s income, consistent with existing Tax Updates.

The CARES Act avoids the above two TCJA limits for accrual to cash conversions for 2019. It suspends the excess business loss limitation for the years 2018, 2019 and 2020. It then not only waives the 80% income limit of a net operating loss (NOL) carryover but allows NOL carrybacks to the five prior tax years if there is taxable income available in those five years. The tax benefit of the NOL could be significantly enhanced by using the higher rates that applied in the pre-TCJA years. For example, prior C Corporation rates of 34% could apply compared to the current 21% rate. These provisions are particularly relevant for multistate taxpayers from a SALT Tax perspective.

The CARES Act NOL carrybacks are currently able to be filed by faxing the NOL carryback form to the IRS. This strategy is open only to 2019 forms tax returns that have not yet been filed. No provisions have yet been passed that would allow an amended return to change an already filed 2019 or 2018 tax return to adopt the cash method.

The IRS has encouraged the availability of the use of the cash method for small businesses over the years with measures including Revenue Procedure 2001-10 that allowed businesses with receipts of less than $1 million to adopt the cash method if they accounted for inventories. Revenue Procedure 2002-28 increased the average gross receipts threshold to $10 million for selective types of businesses.

The TCJA cleaned up these Revenue Procedures by enacting the following rules for businesses starting in 2018: (1) revised IRC Sec. 448 to allow C Corporations or partnerships which have a C Corporation partner to use the cash method of accounting if average gross receipts did not exceed $25 million; (2) added IRC Sec. 471 (c} to allow small businesses that met the IRC Sec. 448 $25 million average gross receipts test to treat inventory as (a) non-incidental materials and supplies or (b) conform to their applicable financial statements or books and records prepared in accordance with their accounting procedures; and (3) added 263A(i) to exempt these small businesses with average gross receipts not exceeding $25 million from being subject to the 263A Inventory Capitalization rules.

Other details to keep in mind with the TCJA rules are aggregation rules based on single employer rules under IRC Sec. 52 (a) and (b) that make it easy for affiliates to be brought into the testing group for the $25 million average gross receipts. To utilize the TCJA rules, it is essential for all owners to stay abreast of the ownership positions. Also, tax shelters are not allowed to use the cash method per 448(a)(3), which in turn are not allowed to use 471(c). Tax shelters include syndicates per IRC 461(i)(3)(B). Syndicates are defined under IRC 1256(e)(3) as any partnership or other entity (other than a corporation which is not an S Corporation) if more than 35% of the losses of such entity during the taxable year are allocable to limited partners.

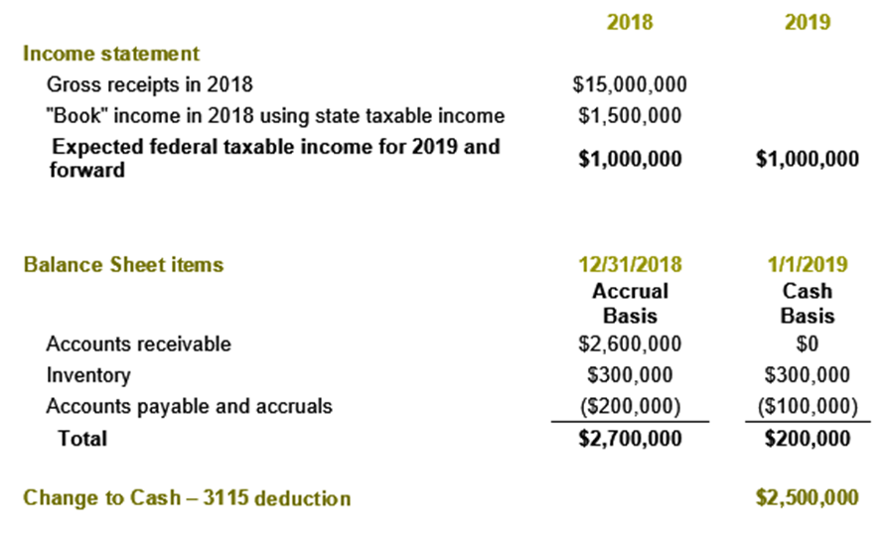

A company has been in business for over two decades. In 2018, it had $15,000,000 in gross receipts and net income of $1,500,000. The net income is based on its state taxable income using the accrual method. Its state does not allow bonus depreciation or extensive use of Section 179. At December 31, 2018, its balance sheet showed that it had $2,600,000 in accounts receivable, $300,000 in inventory, and $200,000 in accounts payables and accruals. It has some manufacturing and assembly involved in the products that it sells to its customers, which are primarily larger companies.

As it considers it alternatives before preparing its 2019 tax return, the company notes that with its average gross receipts of less than $25,000,000, it qualifies for the recently passed TCJA IRC Sec. 471(c} and that it could make an accounting change to cash except for its current method of accounting for inventories. After the change it would have no accounts receivable, would retain its inventory of $300,000 and would reduce its accounts payable to the $100,000 connected to its inventory. The adjustment to cash would result in filing Form 3115 with a $2,500,000 deduction on its 2019 tax return.

In considering its alternatives, the company anticipates that it will generate $1,000,000 of federal taxable income in 2019 and over the next several years.

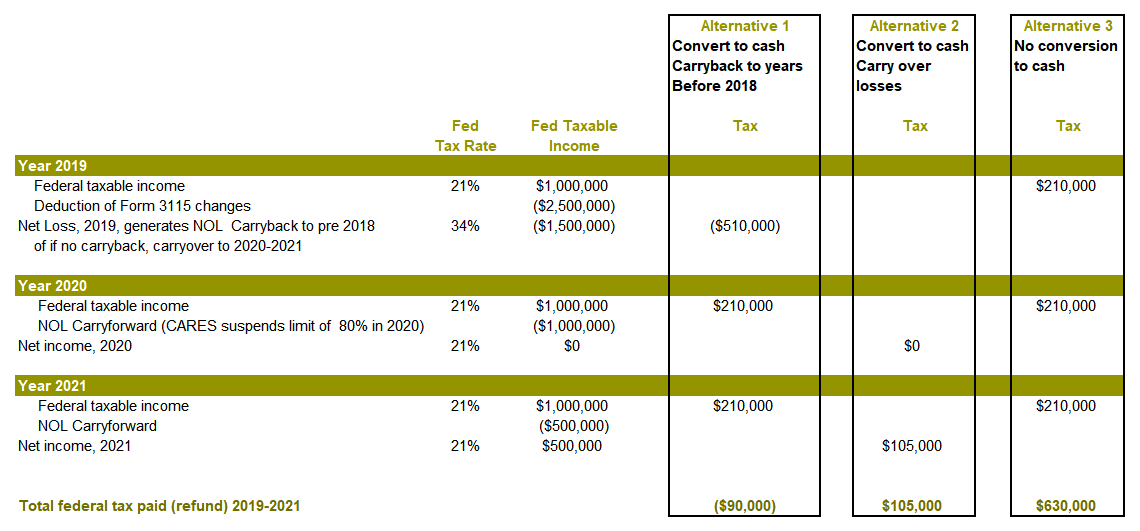

See attached worksheet. The results are most easily compared by looking at the tax refunded or paid out over the years from 2019 through 2021 when any carryover would be fully utilized. Comparisons are made as follows:

The company could also be a pass-through business (an S Corporation or partnership) or a sole proprietorship and the cash conversion provisions of the TCJA and carryback provisions of the CARES Act would both apply. Please note the following based on the example of the company: